Overview: Alphabet clears the $400 billion mark

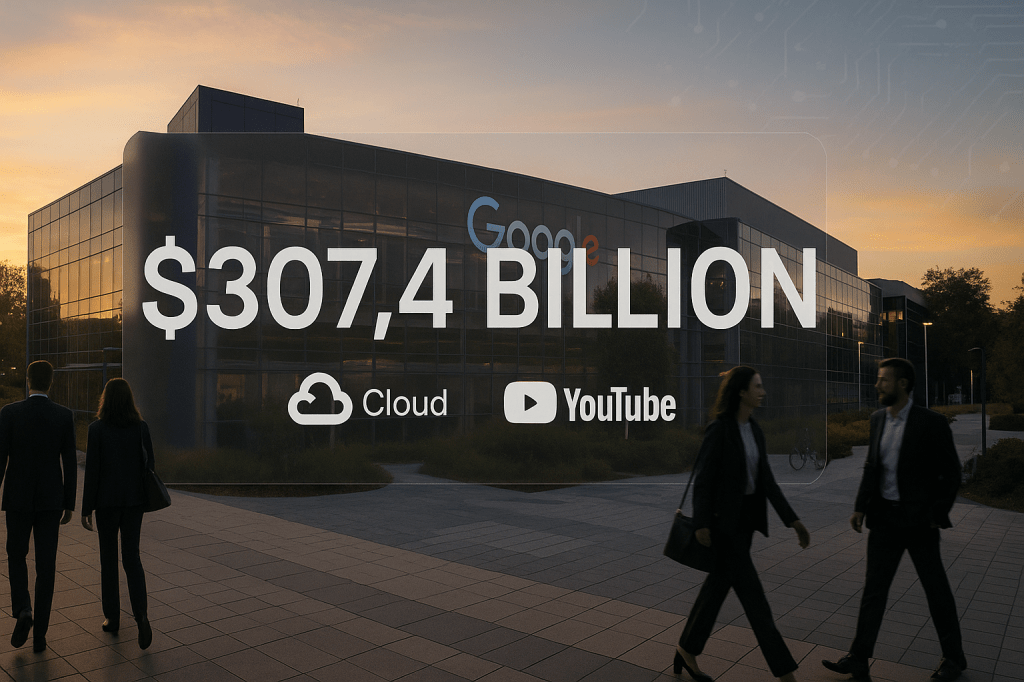

Alphabet, the parent company of Google, reported annual revenue above $400 billion for the first time after its Q4 2025 results. The company posted 15 percent year over year revenue growth, driven by strong performance in Google Cloud and YouTube. Google Cloud reached a $70 billion run rate in 2025, and YouTube generated more than $60 billion from ads and subscriptions.

These figures matter to ordinary users because they shape where Google invests next. Increased cash flow can fund new AI features, influence product design across search and mobile services, and affect pricing for ad supported products and subscriptions.

Why this milestone matters

Hitting more than $400 billion in annual revenue is a corporate milestone. For investors, it signals that Alphabet has returned to sustained growth, at least for the recent year. For users, it means Google has resources to continue investing in artificial intelligence, cloud infrastructure, and creator tools on YouTube.

Quick definitions for readers

- Run rate, plain language. Run rate is a way to estimate annual revenue by taking recent results and projecting them forward. A $70 billion run rate for Google Cloud means recent revenue scaled over a year would reach about $70 billion.

- Google Cloud. This is Google’s set of products and services for businesses, including cloud computing, data services, and AI tools.

- Gemini. Google’s family of large language models that power AI features in search, Workspace, and other products.

Where the 15 percent growth came from

Alphabet’s 15 percent year over year increase reflects gains across multiple business units. Two clear drivers were cloud adoption by enterprises and continued growth in video advertising and subscriptions on YouTube.

Key contributors included:

- Google Cloud expansion, driven by enterprises buying infrastructure and AI services.

- YouTube ad sales and paid memberships, including Shorts and longer form video ad formats.

- Search ad demand and monetization across mobile and desktop search results.

Google Cloud: $70 billion run rate and what that implies

Google Cloud reaching a $70 billion run rate is a notable achievement. It shows continued enterprise demand for infrastructure, managed services, and AI tooling. Cloud customers buy compute that runs applications, stores data, and supports machine learning workloads.

What this means in practice:

- Revenue growth gives Google more room to invest in datacenters, networking, and specialized AI chips.

- Competition remains intense. Amazon Web Services and Microsoft Azure remain the largest rivals, and price and feature competition will stay active.

- Profitability and margins matter. Run rate measures scale, but investors will watch whether Cloud contributes improving margins over time.

Enterprise demand and margins

Enterprises are buying more cloud capacity to run AI workloads, which often need large amounts of compute. That demand helps revenue, but high infrastructure costs can pressure margins. How Google shifts spending toward efficient data centers and specialized hardware will affect future profitability.

YouTube: more than $60 billion from ads and subscriptions

YouTube passing $60 billion in combined ad and subscription revenue highlights the platform’s role in the creator economy and media advertising. That total includes ad sales on long form videos, Shorts monetization, and paid products like YouTube Premium and channel memberships.

Growth drivers include:

- New ad formats and improved targeting powered by AI; these can raise ad prices and ad effectiveness.

- Subscriptions and direct payments that diversify revenue beyond ads.

- Investment in Shorts and creator monetization features that encourage more content and viewer time.

AI investments and what stronger cash flow enables

Alphabet’s strong cash flow creates room to invest in artificial intelligence research and product development. That includes work on Gemini, AI features in Search and Ads, and new tools for Workspace and consumer apps. The company can also pursue acquisitions that help fill technology gaps.

For everyday users, that could mean smarter search results, AI writing helpers in email and documents, and more personalized features across apps. For businesses, it can mean new managed AI services and tools that reduce the complexity of deploying models.

Investor and market implications

For investors, the $400 billion milestone matters for valuation, expectations, and allocation of capital. Analysts will watch upcoming quarters to see if growth stays consistent and whether Cloud margins improve. Strong results give Alphabet flexibility to return cash to shareholders, fund buybacks, or invest in strategic areas.

Regulatory and competitive risks

Big revenue and market reach do not remove scrutiny. Alphabet remains subject to antitrust reviews in multiple countries, and privacy regulation continues to shape how ad targeting works. Competition comes not only from Amazon and Microsoft in cloud services, but also from Apple in consumer devices and from AI focused startups in model development.

Regulatory and privacy changes could affect ad revenue over time. That is one reason observers pay attention to how Google balances AI development with user privacy protections.

How this could affect consumers

Here are likely consumer level implications based on the earnings and stated priorities.

- Improved AI features across Google products. Users may see more integrated AI in search, email, and maps.

- Ads and subscriptions. Google may continue to push combined ad and subscription products, giving users choices between ad supported features or paid, ad free experiences.

- Product experimentation. With more revenue, Google can trial new services and rollout AI driven capabilities more quickly.

Near term outlook and key questions

Several near term questions will shape Alphabet’s next few quarters.

- Can ad growth remain strong if privacy rules tighten? Changes to tracking and targeting could dampen ad revenue over time.

- Will Google Cloud convert scale into higher margins? Investors will monitor whether cloud profitability improves as revenue grows.

- How will AI investments translate into revenue? Launching new AI driven products is one step; converting them into meaningful sales is another.

Suggested visuals and sidebars for readers

- Revenue breakdown chart. Show annual revenue by segment: Search, YouTube, Google Cloud, Other Bets.

- Cloud run rate explanation. A brief sidebar that shows how run rate is calculated using recent revenue figures.

- YouTube monetization timeline. A short timeline showing key moments such as ad formats, Premium launch, Shorts monetization.

Key takeaways

- Alphabet reported annual revenue above $400 billion for the first time, with 15 percent year over year growth.

- Google Cloud reached a $70 billion run rate, signaling strong enterprise demand and ongoing competition with AWS and Microsoft Azure.

- YouTube generated over $60 billion from ads and subscriptions, supported by new ad formats and paid features.

- Strong cash flow supports continued investment in AI, including Gemini and product integrations, while regulatory and competition risks remain.

FAQ

Is the $400 billion figure revenue or profit?

That number refers to annual revenue, not profit. Revenue is total money earned from sales and ads. Profit is what remains after costs and expenses.

What is a run rate and why does it matter for Cloud?

Run rate projects full year revenue using recent results. For Cloud, a $70 billion run rate indicates the scale of current business, but it does not guarantee future profit margins.

Will Google raise prices for consumers because of these results?

There is no direct evidence that consumers will face immediate price increases. The report suggests Google has more resources to invest in products, and the company can choose how to balance free, ad supported options and paid subscriptions.

Conclusion

Alphabet reaching more than $400 billion in annual revenue is a major milestone that reflects growth across Google Cloud and YouTube. For users, the main takeaway is that Google can continue to fund AI research and new product features. For investors and regulators, the focus will shift to whether that growth can be sustained, whether Cloud can improve margins, and how Google navigates competition and privacy rules.

The next quarters will reveal how deeply AI will be woven into Google’s services and whether the company can convert its scale into lasting profitability and user benefit.

Leave a comment